An Andhra Pradesh rent agreement is a legally binding contract between a landlord and tenant that outlines rent, duration,...

A business of one’s own is an unmatched asset. In a developing country like India, ample opportunities are available for both Indian and foreign investors. Some studies have revealed that the primary reason behind people refraining from going ahead with their dream of starting a company is that they are almost clueless about the procedures and protocols involved.

We’ve been there and we’re here to tell you that not knowing the facets of something should never stop you from pursuing your dreams. If you start a new business, you in turn become the backbone of our country’s economy. This article is intended to guide and educate all you would-be entrepreneurs out there.

We’ve tried to prepare an outline of all the steps involved in setting up a startup and the formalities involved. Please bear in mind that the information provided here is of advisory nature alone.

Before we begin let us revisit the very definition of a business. A business enterprise is any institution that engages in the act of production/distribution/maintenance of goods or services to acquire profits and in general, wealth. Acts of distribution come under the domain “commerce” and production comes under the domain “industry”.

A blueprint (a.k.a. the business plan) of the company’s plan is every entrepreneur’s bible. Each entrepreneur must have a blueprint ready before he/she proceeds any further. The blueprint is basically a document with a clear business plan description. It is formally written and often forms the biggest basis for planning everything else. The document is sometimes presented to investors to show them what you plan to do in the future of your company.

Here’s what a typical business blueprint must contain-

In short, the blueprint shall present the vision and strategy of the business in a formal manner.

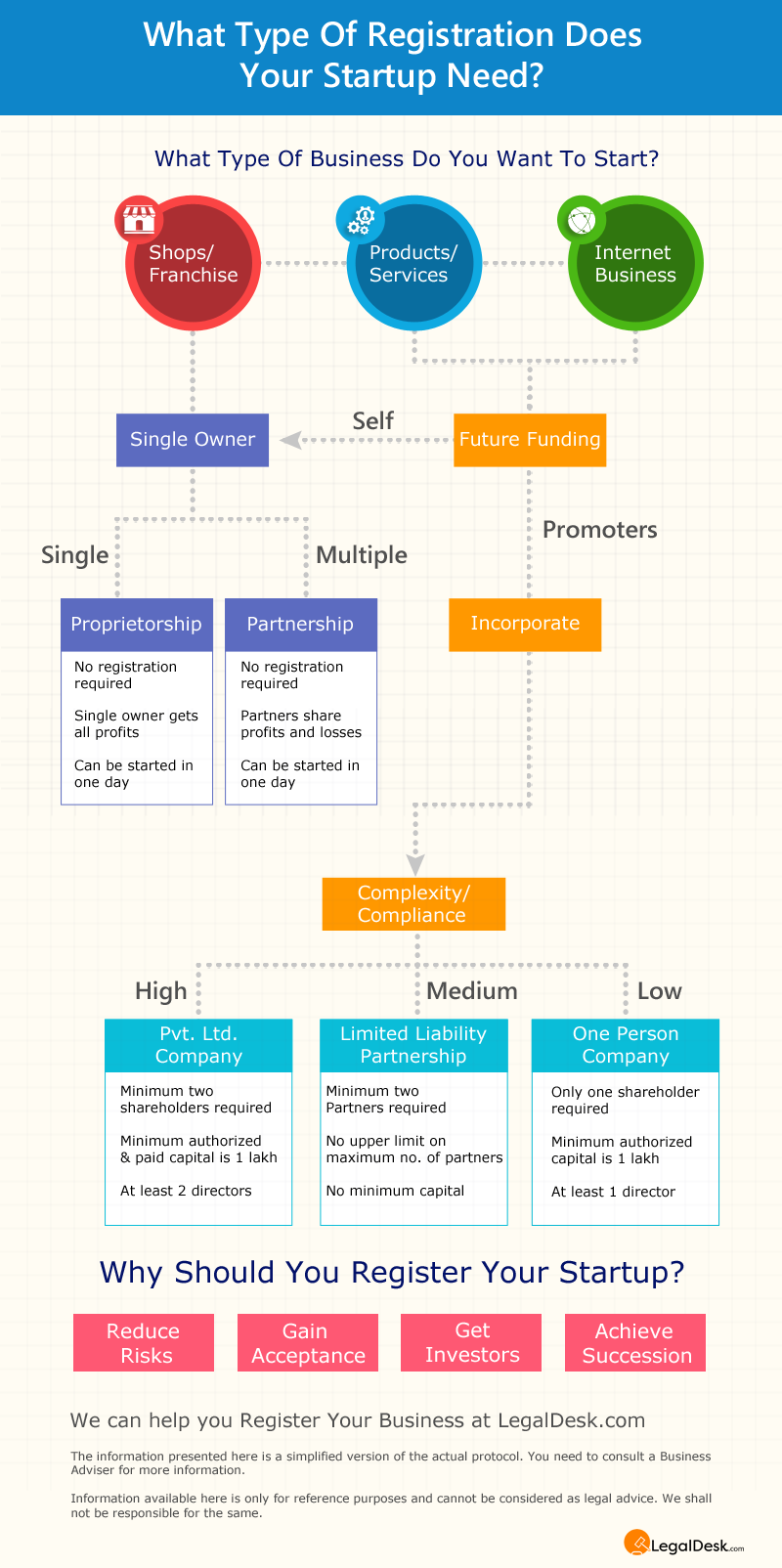

Every entrepreneur must have a basic understanding of the various types of business institutions that our country recognizes. The process of registration and other formalities/regulations for each type of entity is different. Before selecting a type for your business, you need to consider factors like number of members, initial investment etc. Based on such factors, you can register your business are one of the following.

Sole Proprietorship: In sole proprietorship business entity, a single individual owns the entire institution. All the profits and losses are borne by the owner alone. As of now there is no separate law to govern the functioning of such a business.

Partnership: This is a type of business organization where two or more individuals own and share the profits of the company. Every partner is expected to contribute to all aspects of the business and such an organization is governed by the Partnership Act 1932. A partnership agreement should be drafted and signed by all the individuals who possess ownership. Such a document is a written legal agreement between partners.

One Person Company: This is a fairly recent concept, incorporated in 2013, to be precise. In this type of business, one shareholder is allowed to incorporate a private limited company with only a single director. Considered ideal for proprietors who wish to provide a firm structure to their business. OPC has more operational freedom as compared to other types of companies and it needs to hold only two (2) board meetings in a given year.

OPC like other Pvt. Ltd. companies requires a capital of one lakh (1,00,000) and if the turnover exceeds two crores or if the capital goes beyond fifty lakhs (50,00,000), OPC will have to be converted to a Public Ltd. company.

Limited Liability Partnership: In an LLP, there will be at least one (1) member with unlimited liability while the liability of the other members are limited to the extent of their contribution to the organization. An LLP, unlike typical partnership businesses, does not get terminated following the death or insolvency of limited partners. Such organizations are governed by the LLP Act of 2008.

Private Limited Company: This business organization limits the right of shareholders to transfer their shares to others. A minimum of two (2) and a maximum of fifty (50) are allowed to be members and none of the members hold the right to invite the public subscribe to their share capital. And finally Pvt. Ltd Company must have a minimum paid up capital of INR 1,00,000 or more.

Public Limited Company: Public Ltd. Companies bestow their members with the complete right to transfer their shares. Such organizations require a minimum of seven (7) members and places no limit of the maximum number of members. The company can invite the general public to subscribe to their share capital and will have a minimum paid up capital of INR 5,00,000 or more.

Unlimited Company: In this type of business entity the liability of all the members are unlimited. This business entity can be re-registered as a limited company at any time. But as long as it remains as an unlimited company, each member can use their personal assets to settle debts or other similar issues.

Cooperatives: Cooperatives are voluntary organizations which work towards achieving/promoting common interests of its members. Such businesses place no restrictions on the entry or exit of its members. Cooperatives are governed by Cooperative Society Act 1912.

Joint Hindu Family: This is a form of business owned and carried out by the members of a single family. Only the members of the family can manage this form of business which is governed by the Hindu Law.

The process of registering a company in India is quite lengthy and the very reason why people procrastinate. We want our readers to understand that this is only a one time process and the long term benefit definitely makes it worth the effort.

We’ve put together a basic outline of how the registration process of a company must proceed. Keep in mind that some rules are state specific and are bound to change depending of the state in which you apply for. The procedure may also vary based on the type of business. However, most of the steps are same for most types of business.

Please note that many of these steps are optional for proprietorship and partnership firms.

This is the first step in registering your company. Visit the website of Ministry of Corporate Affairs (MCA) and download a DIN application form. It should be issued immediately. Fill this form, attach a copy of your ID proof and address proof and courier it to the MCA for approval. It may take upto 4 weeks to receive the approval.

If you want to make use of e-filing system, you need to get the Class II DSC either directly from MCA or from one of its six authorized agencies, e.g. TCS. Filled application forms can be submitted to the agencies as well.

This must be done electronically. If you have a name in mind, check the MCA website to find out if the desired name is available or not. If it is available, you need it to reserve it with the Registrar of Companies (ROC). Submit an application for reserving desired company name and if it is available, the senior officer at ROC will approve it.

Entrepreneurs should submit their request for stamping the incorporation documents along with the payment receipt, Articles of Association and unsigned copies of the memorandum. These documents should be submitted to select banks or to the Superintendent of copies. Stamp duty may vary from state to state.

This is not a legally mandated rule. This is however a requirement nonetheless to operate your business and is vital when it comes to validating company shares.

Application for PAN can be done through the Internet, however the documents for proof will have to be physically submitted. This can be done at one of the authorized agencies.

Tax Account Number is a number required by anyone collecting or deducting tax. It is a 10 digit alphanumeric sequence. You can look up on the website of income tax to find out about locations where TAN can be applied for.

In addition to the above steps, there are a few other miscellaneous steps that an entrepreneur needs to do in order to start new business in India. They are registrations at the following-

We offer business registration services at LegalDesk. Please contact us today and we will help you kickstart your exciting journey!

We also have many pre-drafted, ready-to-use legal documents such as partnership deeds, agreements, affidavits and other common legal agreement. For your convenience, here’s a list of legal drafts (ready-to-use) available with LegalDesk.

Good luck with starting your own business and holler at us if you need anything. Cheers!